Stablecoins—digital tokens pegged to fiat currencies or other assets—have evolved far beyond crypto curiosities. Today they represent a critical battlefield in the U.S.–China competition for influence over global monetary systems.

1. What Are Stablecoins?

A stablecoin is a cryptocurrency designed to maintain stable value by being backed 1:1 with assets like U.S. dollars, gold, or government bonds (Atlantic Council). Market capitalization reached roughly $240–260 billion in 2025, dominated (83%) by U.S.-based issuers such as USDT and USDC (BeInCrypto).

2. U.S. Strategy: Regulatory Clarity and Dollar Dominance

In March–July 2025, the U.S. advanced and enacted the GENIUS Act, establishing a comprehensive federal stablecoin framework: full asset backing, audits, consumer protections, and issuance controls (Wikipedia). Proponents argue this strengthens the U.S. dollar’s position and draws institutional participation, while critics warn of risks like tax evasion, pseudo-anonymity, and fragile liquidity (washingtonpost.com).

3. China’s Response: Digital Yuan and Regulatory Counters

China regards U.S. dollar-backed stablecoins as a strategic threat. Former central bank officials warn they may deepen dollarization, undermining China’s monetary sovereignty (scmp.com). As a response, China is pushing faster development of its digital yuan (e‑CNY) and exploring offshore yuan stablecoins—especially in Hong Kong as a regulatory sandbox (cryptonews.com).

4. Hong Kong’s Role: A Testing Ground

Hong Kong passed its Stablecoin Ordinance in May 2025, effective August, marking the city as a gateway for yuan-based stablecoins under strict reserve and licensing rules (Forbes, techinasia.com, Coinlive, Cointelegraph). Fintech firms raised over $1.5 billion recently to build stablecoin infrastructure, while equities tied to Hong Kong issuance saw a market correction viewed by experts as healthy rebalancing (Reuters).

5. Strategic Stakes: Beyond Payment Rails

While some see stablecoins primarily as crypto tools, their broader implications include:

Increasing demand for U.S. Treasurys, potentially lowering borrowing costs; issuers such as Tether already hold billions in U.S. government debt, influencing yields (arxiv.org).

Competition between Project Agorá (Western‑led digital payments infrastructure) and mBridge (Asia‑led via central banks) illustrates the infrastructure divide (ft.com).

China’s push for yuan-based systems is part of its broader ambition to shift global finance from the dollar zone (thediplomat.com, ccn.com).

6. Key Tensions & Perspectives

Issue

U.S. Perspective

Chinese / Hong Kong Perspective

Currency Influence

Reinforce dollar‑based global finance

Counterbalance via yuan‑pegged systems

Regulatory Approach

GENIUS Act: streamlined licensing & audits

Hong Kong pilot regime; tight compliance

Sovereignty & Control

Encourages market competition

Prioritizes state control over value flow

Financial Stability

Concern over liquidity stress & bank runs

Risk of USD stablecoin dominance in Asia

7. What’s Next?

U.S.: Implementation of GENIUS enforcement, audit regimes, and integration with Wall Street players like Meta, Visa, Bank of America (BeInCrypto, Business Insider).

China/Hong Kong: Launch of yuan‑pegged stablecoins via state‑backed firms like Ant Group, North King, and testing via Hong Kong compliance regime (Cointelegraph, cryptonews.com, Cointelegraph, Reuters).

Global Competition: EU and UK exploring euro‑based alternatives under MiCA and FCA frameworks, pushing for multipolar stablecoin networks (axios.com, onchainstandard.com).

Conclusion

Stablecoins now stand at the crossroads of global finance and geopolitics. The U.S. seeks to institutionalize dollar-backed tokens under a regulated framework, while China accelerates its national digital currency ambitions through yuan alternatives. Whether stablecoins emerge primarily as financial tools or geopolitical instruments depends on how these systems evolve—and which financial blocs gain the trust of global markets.

In today’s digital era, financial technology—or Fintech—is revolutionizing the way we interact with money, banks, insurance, and investments. Whether you’re tapping your phone to pay, buying crypto, or using a robo-advisor to manage your portfolio, you are participating in the fintech revolution.

But fintech in 2025 is not just about convenience—it’s about financial inclusion, efficiency, and global access to trusted and secure financial systems. Let’s explore what fintech means today and where it’s headed.

What is Fintech?

Fintech is the fusion of finance and technology, designed to streamline, automate, and improve the delivery and use of financial services. It disrupts traditional financial systems by offering faster, cheaper, and more inclusive alternatives.

Today’s key fintech verticals include:

Digital Payments: Mobile wallets (e.g., Apple Pay, Google Pay), QR payments, and instant transfers

2010s: Rise of smartphones → mobile banking, P2P payments, robo-advisors

2020–2023: Surge in blockchain, digital assets, open banking, and fintech superapps

2024–2025: Emergence of DeFi, embedded finance, CBDCs, and AI-native banking

Fintech is no longer a niche—it’s the new face of mainstream finance.

Core Technologies Powering Fintech

The fintech industry now relies on powerful, emerging technologies:

1. Artificial Intelligence (AI)

AI enables predictive analytics, fraud detection, and personalized financial planning

Example: ChatGPT-like financial assistants integrated into banking apps

AI helps banks cut operational costs by automating underwriting, risk assessment, and customer support

2. Blockchain & Web3

Enables secure, immutable financial transactions

Powers Decentralized Finance (DeFi) platforms like Aave and Compound

Supports tokenization of real-world assets (e.g., property, artwork, bonds)

3. Big Data & Predictive Analytics

Transforms raw financial data into actionable insights

Helps in credit scoring, insurance risk modeling, and market trend analysis

4. APIs & Open Banking

Open banking mandates allow third-party apps to access bank data (with user consent)

Fintechs use APIs to deliver aggregated financial dashboards, multi-bank insights, and smart budgeting tools

5. Central Bank Digital Currencies (CBDCs)

Pilots in China (e-CNY), Singapore, Nigeria, and soon Europe

Promotes government-backed, programmable digital currencies

Latest Trends in Fintech

🌐 1. Embedded Finance

Financial services are now integrated into non-financial platforms—you can buy insurance while checking out online or get instant credit inside a ride-hailing app.

Examples:

Grab integrating loans and insurance in Southeast Asia

Shopify offering merchant loans at checkout

🏦 2. Rise of Neobanks and Fintech Superapps

Neobanks offer app-only banking experiences with no branches, low fees, and real-time analytics.

Superapps like WeChat and Gojek combine banking, payments, shopping, and investments all in one platform.

🤖 3. AI-Native Banks

Banks are being rebuilt from the ground up with AI as their core engine. Personalized investment advice, real-time alerts, and smart assistants are standard features.

💱 4. Real-World Asset (RWA) Tokenization

Tokenizing physical assets (e.g., real estate, collectibles, commodities) onto blockchain platforms increases liquidity and accessibility.

Example: BlackRock and JPMorgan are experimenting with tokenized asset funds on blockchain.

🔐 5. Fintech + Cybersecurity

Due to growing data privacy concerns, fintech firms are adopting zero-trust architecture, biometric authentication, and decentralized identity management to enhance security.

Regulatory Uncertainty: Global variation in digital asset and lending rules

Cyber Threats: Increased sophistication of financial fraud and phishing

Interoperability: Ensuring seamless integration across platforms and borders

Trust Building: Many users remain wary of fully digital financial services

What’s Next?

As we look forward:

DeFi may challenge traditional finance with borderless, permissionless systems

CBDCs will reshape how nations think about monetary policy and remittances

AI + Blockchain fusion could lead to smart, self-executing financial products

Sustainability-focused Fintech will rise, combining green finance with impact investing

Final Thoughts

The fintech revolution is not slowing down—it’s accelerating. As new technologies emerge and regulations mature, the financial world will become more inclusive, intelligent, and decentralized.

Whether you’re a student, investor, entrepreneur, or policymaker, staying updated with fintech trends is no longer optional—it’s essential.

🚀 Welcome to the future of finance. It’s digital, decentralized, and designed for everyone.

In today’s digital age, the financial world is evolving at an unprecedented pace. The convergence of financial technology (fintech) and stablecoins is creating new opportunities for inclusion, efficiency, and innovation. From decentralized finance (DeFi) and cross-border payments to programmable money and regulatory sandboxes, this transformation is reshaping the global financial system.

This article explores how fintech and stablecoins are building a more resilient digital economy—and how countries like Malaysia, Singapore, and Hong Kong are positioning themselves at the forefront.

💡 What Is Fintech?

Fintech refers to the use of digital technologies to enhance, automate, or reinvent financial services. It spans everything from mobile banking and digital wallets to blockchain, AI-based risk scoring, robo-advisors, and beyond.

🚀 The Evolution of Fintech:

Fintech 1.0: Telegraphs and ATMs marked early automation.

Fintech 3.0: Smartphones enabled peer-to-peer payments and crypto adoption.

Fintech 4.0: Today’s innovations include Web3, artificial intelligence, DeFi, and stablecoins.

Fintech democratizes access to finance and streamlines services across sectors, especially in underserved markets and emerging economies.

💳 Digital Payments: A Global Shift

The move toward cashless economies is accelerating. Digital wallets, QR code payments, and contactless transactions are becoming the norm.

📱 Popular Wallets: Apple Pay, Google Pay, Alipay, Touch ‘n Go, WeChat Pay

🌐 Growth: Over 60% of global e-commerce payments are expected to be made via digital wallets by 2026.

This shift enhances convenience, lowers transaction fees, and supports financial inclusion—especially in rural and mobile-first regions.

🔗 Blockchain and Decentralized Finance (DeFi)

Blockchain technology provides the foundation for decentralized systems that are secure, transparent, and resistant to tampering.

It powers:

Cryptocurrencies like Bitcoin and Ethereum

Smart contracts that self-execute financial logic

DeFi platforms for lending, borrowing, and trading without intermediaries

Together, blockchain and DeFi are redefining how finance is conducted—offering 24/7, permissionless access to capital.

🪙 What Are Stablecoins?

Stablecoins are digital currencies designed to maintain a stable value, usually pegged to a reserve asset like a fiat currency, commodity, or algorithmic model. They serve as a bridge between traditional and decentralized finance, offering the speed of crypto with the predictability of money.

📌 Why Stablecoins Matter:

Reduce price volatility

Enable global remittances and real-time payments

Power smart contracts and DeFi ecosystems

Act as a store of value in high-inflation economies

🧱 Types of Stablecoins:

Type

Backed By

Examples

Fiat-backed

USD, MYR, etc.

USDT, USDC, FUSD

Crypto-backed

ETH, BTC (overcollateralized)

DAI

Commodity-backed

Gold or other assets

PAXG

Synthetic/Algorithmic

Derivative-based

USDe (Ethena)

🌟 Major Stablecoins in 2025

1. USDT (Tether)

The most widely used stablecoin globally

Pegged to USD, backed by mixed reserves

Ideal for trading, DeFi, and fast settlements

2. USDC (USD Coin)

Issued by Circle; fully backed by U.S. dollar reserves

Highly regulated, widely adopted across platforms

Preferred by enterprises and institutions

3. DAI

Decentralized stablecoin issued by MakerDAO

Collateralized by crypto (ETH, USDC)

Maintained via smart contracts and governance

4. FUSD (Frax USD)

A partially algorithmic stablecoin transitioning to full collateralization

Known for yield-bearing integrations in DeFi

5. USDe (Ethena USD)

Synthetic stablecoin backed by hedging strategies

Offers capital efficiency, gaining traction in modern DeFi

6. PAXG (Paxos Gold)

Tokenized gold asset; each token backed by one ounce of gold

Combines crypto liquidity with physical value

🔧 Real-World Applications of Stablecoins

💰 DeFi Lending and Borrowing

Platforms like Aave and Compound use stablecoins for peer-to-peer lending—offering liquidity, yield generation, and financial access.

🌍 Cross-Border Payments

Stablecoins eliminate FX fees and delays, allowing businesses and workers to transact globally in seconds.

🛒 E-Commerce and BNPL

Buy Now Pay Later services can be built using smart contracts and stablecoins, enabling instant approvals and programmable repayments.

🧾 Payroll and Gig Economy

Freelancers and gig workers can receive salaries in stablecoins, offering fast and borderless compensation.

🏠 Tokenized Real-World Assets

From real estate to commodities, assets are being tokenized and traded using stablecoins as a secure, liquid medium of exchange.

🏛️ Regulatory Highlights & National Projects

Countries are moving quickly to regulate stablecoins while fostering innovation. Here’s how Malaysia, Singapore, and Hong Kong are leading in Asia:

Malaysia – Blox: Ringgit-Based Stablecoin (Proposed)

Blox is a Ringgit-backed stablecoin concept under review by Bank Negara Malaysia (BNM).

It aims to power e-commerce, DeFi, and cross-border payments using a localized, compliant digital currency.

May be tested under Malaysia’s Fintech Regulatory Sandbox.

Seen as a key tool for Shariah-compliant digital finance and boosting financial inclusion.

Malaysia’s cautious but inclusive approach emphasizes domestic utility, compliance, and Islamic fintech potential.

Project Orchid is a stablecoin regulatory framework launched by the Monetary Authority of Singapore (MAS).

It includes requirements for:

1:1 fiat reserve backing

Guaranteed redemption at par value

Transparent audits and disclosures

Encourages real-world applications like:

Government aid distribution

Retail payments

Cross-border enterprise use

Singapore combines policy clarity with fintech openness, making it a launchpad for stablecoin innovation.

Hong Kong – Institutional-Grade Licensing

The Hong Kong Monetary Authority (HKMA) is developing a licensing framework for fiat-referenced stablecoins.

Key requirements include:

Full reserve backing in high-quality liquid assets

Monthly reporting and third-party audits

Strong cybersecurity and risk management

Part of a broader Web3 strategy to attract institutional capital and support regulated virtual asset providers (VASPs).

Hong Kong is shaping a rigorous, compliance-driven framework targeting institutional finance and enterprise adoption.

🌏 Regional Overview

Country

Strategy Focus

Status

Use Cases

Malaysia

Local fintech & DeFi

Conceptual/Pilot

MYR stablecoin, e-commerce, DeFi

Singapore

Innovation & Regulation

Active Implementation

SGD stablecoins, enterprise payments

Hong Kong

Institutional oversight

Licensing in progress

Regulated stablecoins for Web3 finance

🔮 What’s Next for Fintech & Stablecoins?

The future of digital finance is taking shape through several trends:

🔁 Interoperability

Cross-chain bridges and Layer-2 solutions are making stablecoins usable across ecosystems like Ethereum, Solana, and Internet Computer (ICP).

⚙️ Programmable Money

Smart contracts are enabling programmable payrolls, subsidies, taxes, and grants.

🏦 Institutional Stablecoins

Banks and financial firms are issuing their own stablecoins for B2B use, liquidity management, and compliance.

🌐 CBDC Coexistence

Stablecoins and Central Bank Digital Currencies (CBDCs) will likely coexist—with stablecoins leading in flexibility and programmability, while CBDCs serve core public infrastructure.

🌍 Rise of National Stablecoins

Countries are issuing sovereign stablecoins (e.g., Malaysia’s Blox) to promote currency sovereignty, data localization, and regulated DeFi.

✅ Conclusion

Fintech and stablecoins are more than just buzzwords—they are building blocks of the next financial era. As infrastructure matures and regulations evolve, we are witnessing the creation of a borderless, decentralized, and inclusive financial system.

💡 The financial future will be co-created by governments, developers, and users—with stablecoins at the center of trust, efficiency, and innovation.

Watch this Video to understand more about Stablecoins

In the previous post, you learned about the fundamental concepts of the Internet Computer Protocol (ICP), a third-generation blockchain designed to power the next evolution of the internet. At its core, ICP functions as a decentralized cloud, enabling developers to build and deploy applications entirely on-chain without relying on traditional centralized servers like AWS or Google Cloud.

You might be wondering—how is this even possible? To clear up any doubts, I will walk you through the process of creating and deploying an application on the Internet Computer. Unlike conventional web hosting, ICP allows you to launch apps without registering a domain name or provisioning a cloud server, leveraging blockchain-native web hosting for a truly decentralized experience.

Prerequisite

To start coding in IC(Internet Computer) , there are some prerequisites you need to set up or install before you can jump into developing your first app. Following are the prerequisites:

Ensure you have the supporting operating system-

Windows 10 or 11 with WSL2 installed with Ubuntu Linux v20.04

Mac OSX 12 or above

Ubuntu Linux v20.04

NodeJs v20

GitHub Account

IC SDK

Visual Studio Code IDE

Basic programming knowledge- JavaScript, CSS, HTML

Here are the references to install the or set up the prerequisites:

After installation, check its version using the command dfx –version, you should see something like dfx 0.24.3

*·If you are using a machine running Apple silicon, you will need to have Rosetta installed. You can install Rosetta by running softwareupdate –install-rosetta in your terminal.

The next step is to create an account in IC. In ICP, authentication requires a key pair consisting of a private and a public key, while the account itself is identified by a unique principal ID. Additionally, a ledger is needed to store accounts and transactions. This ledger is a smart contract known as a system canister. Each user will have a ledger account identifier, also called an account ID, which is used to hold ICP tokens. Furthermore, a wallet must be created to store cycles and facilitate sending cycles to and from canisters.

Creating ICP Account

To create an account in IC, using the following command:

dfx identity new <identity_name>

·💡Identity names must use alphanumeric characters comprising uppercase and lower letters, numbers and special characters. Example: My_chatb@t

·ℹ️Most importantly, REMEMBER to back up the 24-word account/identity seed phrase. This is essential for restoring your account if you forget your password or need to access it from another device. Additionally, you can create multiple accounts on your device.

Principal ID

Having created your account, you can obtain your principal id using the following commands:

In case you have changed your device and need to use the same account to develop ICP apps, you may import the 24-word seed phrase you have saved as a plaintext into your new development environment using the following command:

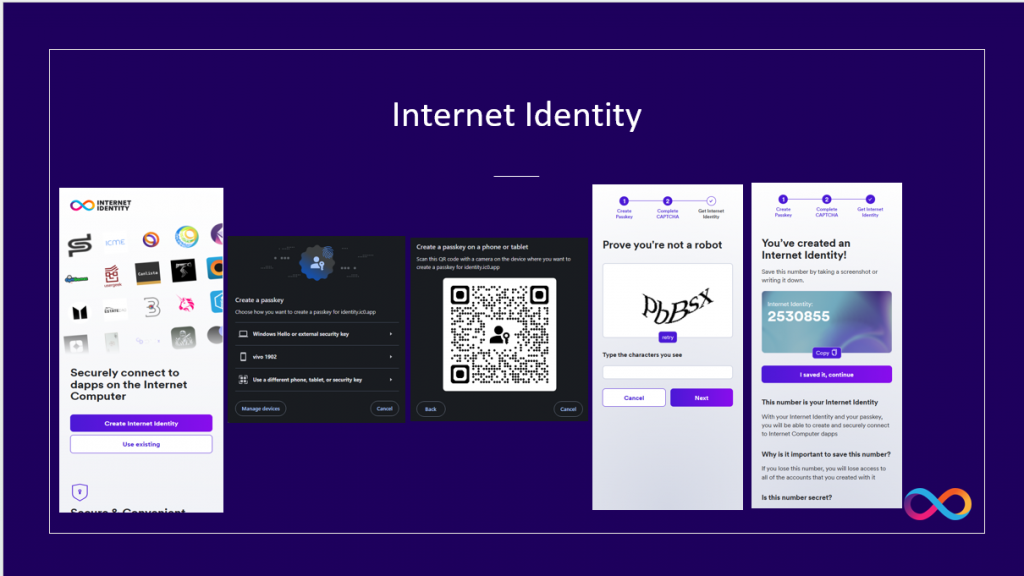

Follow the prompts to register your device . For Windows 10 user, require to use your mobile phone to scan the QR Code to store the credential information in the mobile phone. For Android device, recommend to use Google Lens to perform Passkey QR code scanning.

Note down your Internet Identity number (e.g., 12345).

ICP Account Address

To receive ICP tokens, you need an ICP account address associated with your Internet Identity. Here’s how to get it:

Once logged in, navigate to the “Accounts” section.

Plug Wallet

You may also use the Plug Wallet to store your ICP tokens. Plug wallet can be installed as a browser extension on a laptop or can be installed as a mobile app on your phone. You can download Plug Wallet using the link below.

The Network Nervous System (NNS) is the decentralized governance system aka DAO that controls and manages the Internet Computer (ICP), a blockchain-based computing platform developed by the DFINITY Foundation. The NNS is one of the most critical components of the Internet Computer, as it enables the network to operate autonomously and evolve over time through community participation.

Key Functions of the NNS

Governance:

The NNS allows ICP token holders to participate in the governance of the Internet Computer by submitting and voting on proposals.

Proposals can cover a wide range of topics, such as upgrading the protocol, adjusting network parameters, or funding ecosystem projects.

Token Economics:

The NNS manages the ICP utility token, including its minting, burning, and distribution.

It also handles the creation of cycles, which are used to pay for computation and storage on the Internet Computer.

Node Management:

The NNS oversees the addition, removal, and configuration of node machines that power the Internet Computer.

It ensures the network remains secure, scalable, and efficient.

Canister Management:

The NNS manages the lifecycle of canisters (smart contracts) on the Internet Computer, including their creation, upgrading, and deletion.

Network Upgrades:

The NNS facilitates seamless upgrades to the Internet Computer protocol without requiring hard forks or downtime.

This is achieved through a decentralized voting process.